Forword

The year 2026 marks the opening of China’s 15th Five-Year Plan period, making the automotive sector’s direction a key industry focus. Drawing on twelve analytical dimensions, such as strategic status, development models, market size, core technologies, globalization, and policy environment—EV100 Plus examines and anticipates the new landscape and emerging opportunities for China’s auto industry under the 15th Five-Year Plan, providing valuable insights for industry stakeholders.

1. The Strategic Role of the Auto Industry Continues to Expand

The automotive sector remains a pillar of China’s economy. From January to October 2025, its revenue hit RMB 8.88 trillion, accounting for 9.1% of total manufacturing sector. Retail auto sales exceeded RMB 4 trillion over the same period, making up 9.7% of total consumer goods sales. In the first three quarters of 2025, value-added growth in auto manufacturing reached 11.2%, significantly outpacing real estate (0.6%) and overall GDP growth (5.2%). The industry is now central to both manufacturing and consumption, serving as a key economic stabilizer.

It is also a major driver of China’s globalization. Vehicle and parts exports from January to October 2025 reached RMB 1.36 trillion, up 9% year-on-year and accounting for 6.2% of total exports. Exports of electric passenger vehicles surged 35.6% to RMB 390.1 billion, representing 49% of total vehicle exports and 39% of the “new three” export industries (new energy vehicles, lithium-ion batteries and photovoltaic products), solidifying their role as a core engine for foreign trade.

Furthermore, the automotive sector acts as a convergence platform for technological innovation. Building on the foundation progress in electrification alongside batteries and motors, it is now entering the intelligent ear. Cutting-edge technologies such as semiconductors, AI, and next-gen communications are achieving large-scale application in automobiles, making the sector a primary testing ground for new quality productive forces. The market for intelligent vehicle features is projected to reach RMB 600 billion in 2025.

During the 15th Five-Year Plan period, the industry will deepen its integration with multiple high-tech fields. Core technologies will increasingly spill over into other sectors. Approximately 70% of key components are interchangeable between intelligent vehicles, low-altitude aircraft, and robotics. Automakers and suppliers are accelerating their layouts into robotics, embodied intelligence, and the low-altitude economy. positioning the auto industry as a major engine for broader technological progress and the cultivation of new quality productive forces.

Intelligent driving has become a central arena in global tech competition. China holds an early-mover advantage, while the US and Europe remain committed contenders, making the next five years a critical window. Chinese driver-assistance solutions from companies like Huawei, Momenta, and DEEPROUTE.AI have entered global supply chains of Audi, BMW, Mercedes-Benz, and Toyota, and are expanding with Chinese automakers abroad. In robotaxis, Waymo trails in London and Tokyo, Chinese firms like Apollo Go, WeRide, and Pony.ai are expanding into the Middle East and Europe, shifting competition from indirect to direct confrontation.

New energy vehicles (NEVs) also form a cornerstone of China’s energy transition. With non-fossil power generation expected to exceed 50% of total output by 2030, Vehicle-to-grid (V2G) technology will be critical tool for peak cut and enhancing renewable energy utilization. China’s NEV fleet is projected to exceed 100 million by 2030, with a combined battery capacity over 6 billion kWh, providing massive flexible storage for the power system and generating “1+1>2” effect with renewable energy.

2. The Industry Accelerates Toward a New Model of High-Tech, High profitability and High Value

The traditional model of competing primarily on scale and thin margins is no longer sustainable. First, structural overcapacity and inefficient resource allocation are prominent. In 2024, capacity utilization in China’s auto manufacturing dropped to 72.2% and has continued to fall. Utilization at many state-owned automakers, EV startups, and joint ventures lingers around 60%, significantly below the global benchmark of 75%.

Second, industry profitability remains weak, trapped in a cycle of “more output without more revenue, and more revenue without more profit.” Profit margins have trended downward from 2023 to 2025, falling below historical averages. After dropping to 4.3% in 2024, margins saw a slight recovery to 4.5% in the first three quarters of 2025 yet still trail the 6% average for industrial enterprises.

A widening profitability gap is also evident. Leading NEV players maintain profits through scale and technology, while many traditional automakers face sharp declines. The strategy of “using fuel profits to subsidize EV losses” is proving unsustainable.

Consequently, the industry must shift to a new model centered on high technology, high profitability, and high value. Technology must become the core driver, elevating competition from “manufacturing capability” to “innovation capability.” This new paradigm will be built on integrated software and hardware, rapid iteration, and user co-creation. Future success will depend not on capacity alone, but on building competitive moats through software-defined vehicles, data-driven development, and ecosystem services. Some players may forego vehicle manufacturing altogether, focusing instead on controlling operating systems, algorithm platforms, or chip architectures—reshaping the value chain much like tech giants did in smartphones.

Simultaneously, the relationship between automakers and users is fundamentally changing. As AI integrates deeper into mobility and daily life, products will proactively anticipate and even shape user needs, shifting users from passive roles to demand leaders.

Product development cycles will compress dramatically, from the traditional 5-7 years down to 12-18 months. Core electronic architectures and intelligent systems will become unified platforms capable of continuous evolution via OTA updates—enabling “one system, lifelong evolution.” However, these high-tech demands intensive R&D and rapid iteration, which is unsustainable under persistently low margins. Companies must build a virtuous cycle where technology drives cost reduction and creates high-value output. By optimizing product mix and building full lifecycle service systems, automakers can extend value into multiple scenarios, improving overall profitability and achieving stable returns.

Beyond financial profits, the industry must also earn recognition from capital markets and society for its technological and ecosystem value, and long-term potential. Deep integration with capital markets—leveraging efficient financing and valuation—is essential to sustain the high-investment, high-risk, high-growth cycle required.

Just as Silicon Valley giants like NVIDIA reinvest vast market capital into R&D and ecosystems, China’s auto industry must close the loop linking technology, products, and capital. Relying solely on end-consumer revenue is insufficient. A mature financial environment is crucial to translate technological value into capital value, creating a self-reinforcing virtuous cycle for high-quality, technology-led growth.

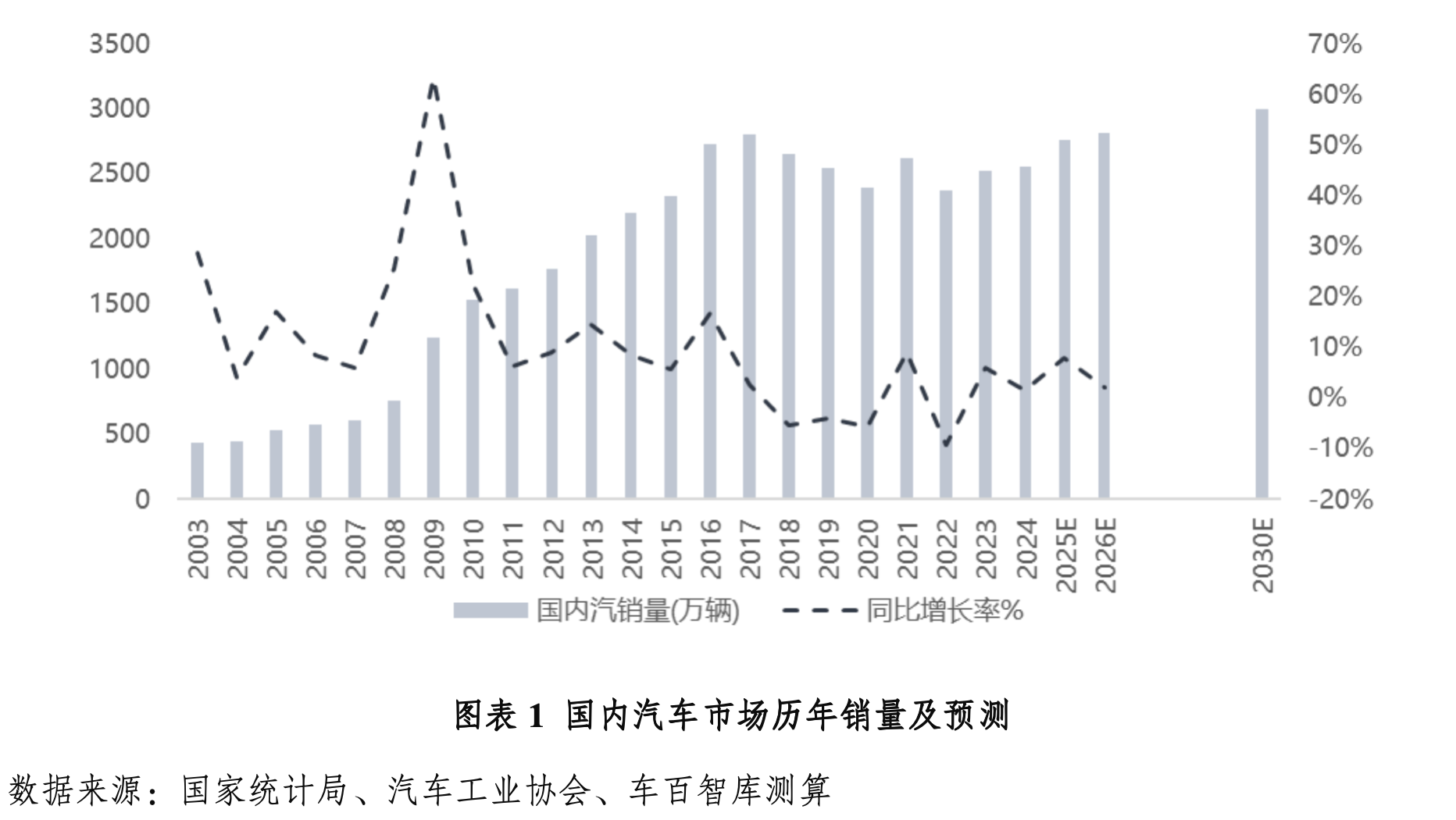

3. China’s Auto Market Enters a Phase of High Sales and Low Growth

China’s auto market has entered a phase of high sales and low growth. From January to November 2025, vehicle sales reached 24.78 million units, a 9.7% year-on-year increase driven by cyclical demand fluctuations. Unlike the high-growth cycle triggered by tax incentives in 2016–2017, the expansion seen in 2025 is expected to transition into a period of stability with modest growth. The industry widely agrees that explosive growth is no longer necessary or sustainable. The key focus is now on avoiding sharp downturns and maintaining long-term stability.

In the short term, assuming an optimistic scenario with orderly policy adjustments (such as “two-new” initiatives) and more standardized competition, China’s auto market is projected to achieve marginal growth of around 2% in 2026, with sales reaching about 28 million units. Over the long term, the domestic market will remain the industry’s core foundation. Growth will be driven mainly by continued consumption support policies and deeper penetration into lower-tier markets. By 2030, annual vehicle sales in China are expected to stabilize at around 30 million units.

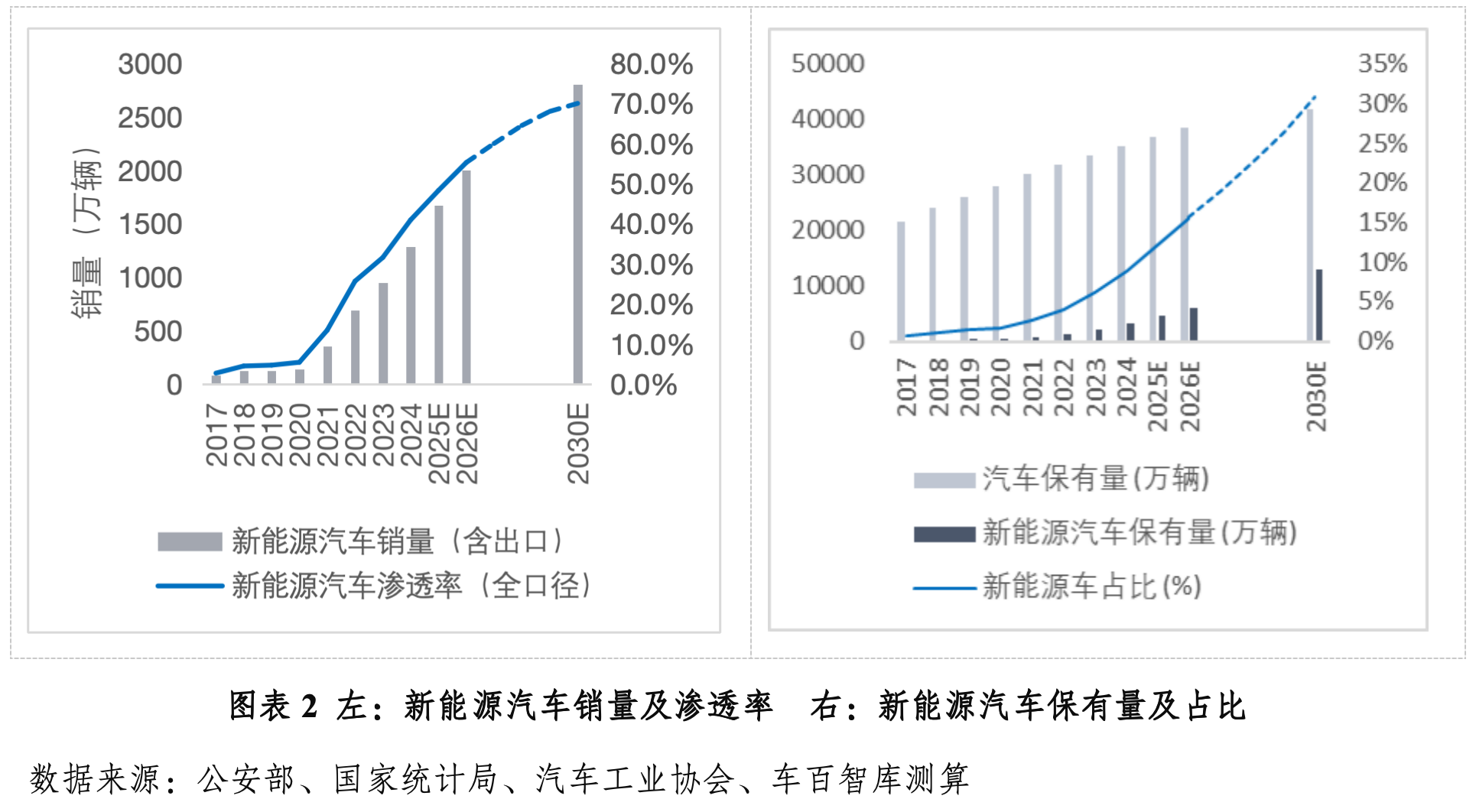

4. Rapid Increase in the Share of NEVs

NEVs will continue to be the primary growth engine for China’s auto industry. From January to November 2025, NEV sales—including exports—totaled 14.78 million units, achieving a penetration rate of 47.5%. Full-year sales are estimated to reach 16.5–17 million units. In 2026, NEV sales are forecast to exceed 20 million units, with penetration rising above 55%.

The proportion of NEVs within the total vehicle fleet has become a key indicator of structural transformation and green development. Unlike sales penetration, which can be volatile in the short term, fleet share more accurately reflects the real pace of transition from “incremental replacement” to “stock conversion.” From a fleet perspective, NEVs still possess substantial growth potential. By the first half of 2025, China’s NEVs had reached 36.89 million units, accounting for 10.27% of all vehicles. By 2026, NEV ownership is expected to surpass 60 million units, raising its share to around 15%. This figure could exceed 30% by 2030.

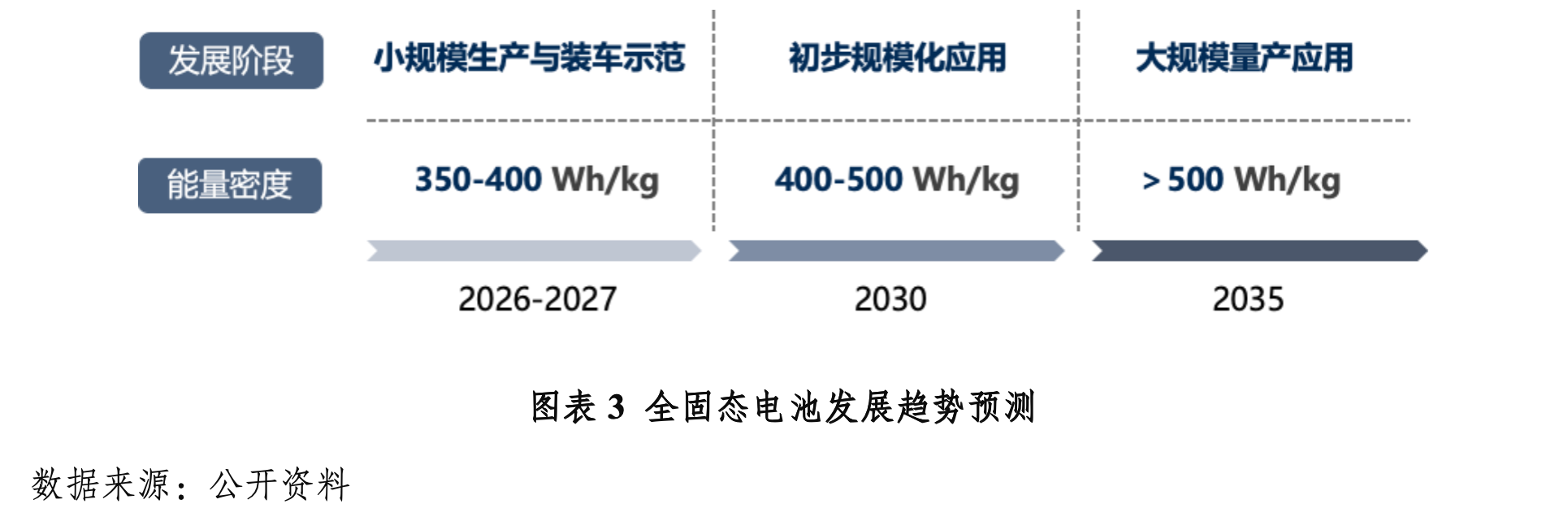

5. Next-Generation Battery Technologies Enter Commercialization

All-solid-state batteries are expected to begin small-batch vehicle deployment within the next two years. Industry efforts are currently converging on sulfide-based systems, with oxide and halide pathways also advancing. Based on current progress, small-scale production and in-vehicle demonstration are likely between 2026 and 2027, with energy density reaching 350-400 Wh/kg. Broader commercialization is anticipated around 2030, with energy density rising further to 400-500 Wh/kg.

The supply chain is accelerating industrialization. For example, Gotion High-Tech’s product has entered pilot production, with a 2 GWh production line under design. In April 2025, SAIC Motor announced its first all-solid-state product, the Guangqi Battery, will launch in 2027.

Sodium-ion batteries are nearing a critical inflection point for scale-up. As materials, processes, and applications mature, a complete ecosystem is forming. In March 2025, HiNa Battery launched a sodium-ion solution for commercial vehicles with energy density exceeding 165 Wh/kg. In November 2025, CATL named Ronbay Technology as its primary cathode material supplier for sodium-ion batteries.

6. Advanced Driver Assistance Systems Achieve Mass Adoption

L2-level driver-assistance systems are becoming widely adopted, with competition intensifying in lower-tier markets. This technology is now a core battleground for intelligent vehicle and a key driver in transitioning China’s NEV industry from the electrification to the intelligence. Automakers and solution providers are collaborating to democratize these features. From January to September 2025, the penetration rate of L2 functions in new passenger vehicles reached 64%. This is expected to rise to 70% in 2026 and 90% by 2030.

Market dynamics are shifting rapidly due to falling costs. The cost of urban NOA (Navigate on Autopilot) is projected to drop from about RMB 10,000 to around RMB 5,000. With vehicles priced under RMB 150,000 representing over half of China’s passenger car market—a segment highly sensitive to value—this price band will become the focal point for urban NOA competition in 2026.

Internal combustion engine (ICE) vehicles remain a major opportunity, still accounting for over half the market. Expanding driver-assistance in these models is a key competitive frontier. In 2026, joint-venture and foreign brands are expected to accelerate the deployment of China-developed solutions in their ICE vehicles to regain market share.

China’s advantage lies in richer functionality and a smoother experience. Traditional L2 systems often offer fragmented features like lane departure warning system, adaptive cruise control, automatic emergency braking, and lane keeping assistance. In contrast, integrated highway and urban NOA systems provide end-to-end assistance, handling complex maneuvers like automated lane changes, ramp navigation, and unprotected turns.

Parking assistance is also evolving quickly, progressing from basic space recognition to automatic parking in familiar spots, memory parking, and autonomous space-finding in complex environments. These upgrades directly address major consumer pain points: locating and effortlessly entering a parking space.

7. Key Technologies of Intelligence Continue to Advance

Computing Power and AI Models are accelerating the AI transformation of vehicles. As cars become more integrated with AI, the mass production of end-to-end models for intelligent driving is sharply increasing the demand for onboard computing.

In intelligent driving, systems in 2025 typically require around 500 TOPS of computing power. As automakers adopt world models and introduce L3 autonomous driving, this demand is expected to rapidly exceed 1,000 TOPS. By 2028, the mass production of L3/L4 systems could push requirements above 2,000 TOPS. Chinese companies are already scaling up with products like Horizon Robotics’s J6P (560 TOPS), Xpeng’s Turing (750+ TOPS) and NIO’s Shenji 9031 (1,000+ TOPS).

In smart cockpits, more powerful chips will enable dedicated, onboard multimodal AI for human-machine interaction. These local models offer lower latency and more immersive experiences than cloud-dependent solutions, with future potential for applications like brain-computer interfaces.

Intelligent chassis systems are emerging as a new competitive frontier, following smart driving and cockpits. As the chassis directly impacts safety and is essential for L3+ autonomy, “by-wire” architectures are becoming the main focus.

New regulations are enabling this shift. China’s GB17675-2025 standard now permits steer-by-wire (SBW), with NIO’s ET9 being the first mass-produced domestic model to feature it. SBW is expected to scale in 2026 alongside L3 pilot programs. Similarly, the updated GB21670-2025 standard allows brake-by-wire systems, with domestic EMB products validated for large-scale deployment starting in 2026.

8. Global Expansion Enters a New Phase of Scale and Upgrading

China’s auto industry is accelerating its global presence. From January to November 2025, vehicle exports reached 6.35 million units (an 8.7% year-on-year increase), with NEV exports doubling to 2.32 million units and becoming the primary growth driver. Full-year 2025 exports are expected near 7 million units.

In the medium term, backed by sustained overseas demand and expanding foreign production capacity, 2026 overseas sales are projected to reach 8 million units (about a 15% year-on-year increase). Overseas production is expected to exceed 1 million units, while NEV exports may rise to about 3.5 million units, implying a two-year CAGR of 60–65%.

Over the longer term, based on top automakers’ capacity plans and major market demand, China’s overseas auto sales are expected to reach about 10 million units by 2030—half of which will be produced and sold locally.

Competitiveness in components continues to strengthen. With lower trade barriers than finished vehicles, auto parts exports are projected to grow 8-10% annually through 2030, reaching USD 160 billion. As global NEV markets expand and battery costs fall, power battery exports alone could reach USD 120 billion, with total parts exports likely exceeding USD 300 billion.

The regional structure of NEV expansion is being reshaped, with the Global South emerging as the main growth engine. Europe remains a high-value market (characterized by high prices, technical thresholds, and brand premiums), but tariffs and carbon-footprint requirements have slowed direct exports. Chinese companies are ramping up “local manufacturing + partnerships + local supply chains,” with over 1.5 million units of annual capacity already built or planned in Europe.

The Global South is becoming the primary battlefield. Customs data shows that from January to October 2025, China exported 1.42 million NEVs to Belt and Road countries—about 70% of total NEV exports. ASEAN leads as a long-term growth market, driven by policy openness and localization. In the Middle East, government procurement, premium demand, and infrastructure investment will drive rapid growth, with EV penetration in the UAE and Saudi Arabia expected to reach 10-15% by 2030. Latin America presents opportunities, with Mexico and Brazil as key markets; from January to October 2025, exports to Mexico reached 483,000 units, making it China’s largest single export destination.

By 2026, China’s NEV overseas sales will shift toward a diversified regional mix centered on ASEAN, the Middle East, and Latin America. Europe will still account for 35-40% of NEV overseas sales and remain a high-value growth market. ASEAN is expected to represent 15-20% as local production ramps up. The Middle East may account for 13-15%, driven by the electrification of taxis, online ride-hailing fleets, and government vehicles. Latin America, led by Mexico and Brazil, is projected to contribute 15-18%.

The overseas model is upgrading to an integrated ecosystem of “vehicles + intelligence + batteries + components + services.” In OEMs, Chinese automakers’ operational overseas plants by 2026 are expected to exceed 2 million units of annual capacity, with planned capacity near 3 million units; the share of overseas production could approach 50%.

In intelligent systems, Chinese firms are exporting digital components and services. Leading companies like Robotaxi operate in markets including Singapore, the UAE, Saudi Arabia, and Switzerland, spanning shuttles, taxis, sanitation vehicles, and mining trucks. Horizon Robotics’s SuperDrive has enabled 25 models from 7 Chinese OEMs to enter major markets across Asia, Europe, the Middle East, South America, and Oceania.

In batteries, overseas capacity is entering a phase of concentrated expansion. As of October 2025, 33 Chinese companies have built, are building, or plan 74 battery and energy-storage manufacturing sites overseas, totaling 811 GWh—meeting about 20% of 2030 global demand projections—with disclosed investment exceeding RMB 387 billion.

In components, globalization is shifting from OEM-led to a supplier-centric model, with suppliers expanding alongside top automakers. By March 2025, the number of Chinese-invested auto parts companies in Thailand had reached 165, up 3.4 times from 2017.

Services are critical to sustainable global profitability. NIO has deployed 61 battery-swap stations across five European countries. Huawei’s liquid cooling fast charging solutions are rolling out across Europe, Southeast Asia, the Middle East, and Latin America. Through long-term operations, energy services, and data-driven models, these platforms boost customer loyalty and brand trust overseas.

9. Multinational Automakers Accelerate Transformation to Adapt to China’s Market

Supporting multinational automakers’ success in China is key to high-level opening-up. These companies stay a vital part of China’s auto ecosystem, contributing significantly to industry scale, market share, and key technologies. Today, around 45 wholly foreign-owned and joint-venture OEMs operate in China, and the country is home to over 100,000 auto parts firms—more than 10,000 foreign-owned or joint ventures—holding over 60% of the high-end passenger car parts market. Multinational firms still dominate areas like automotive electronics, braking systems, fuel injection, and safety systems, so their performance in China shapes not just their own prospects, but the evolution of China’s auto industry.

Multinational brands face growing exit risks as their market share shrinks. In recent years, foreign passenger car brands’ sales in China dropped from 13.19 million units (2020) to 9.27 million (2024)—a nearly 30% decline. Companies with sustained weak performance may be forced to withdraw, making rapid adjustments to their China strategies critical for competitiveness.

“In China, for China” is emerging as the new localization approach. Some multinationals are moving from offshore R&D and decision-making to a “both ends in China” model. Technologically, this means establishing fully localized R&D systems centered on electrification and intelligence—Volkswagen, for example, built its China Technology Center (VCTC) and developed the China-tailored CMP electric architecture.

On the management front, decision-making is drawing closer to the market. Product definition is shifting to frontline teams with deeper insights into local consumers. Chinese teams are taking a growing lead in NEV R&D, with local organizations driving China-market strategies.

A complementary shift — “in China, for the world”—supports China’s global goals. Multinationals can use their global networks, resources, and brands to take China-co-developed innovations global, creating win-win outcomes. They can also help Chinese suppliers expand overseas, creating new routes for the globalization of China’s auto value chain.

10. The Auto Industry Converges with Embodied Robotics and the Low-Altitude Economy

Shared technologies, interconnected supply chains, and overlapping scenarios are driving convergence between automobiles, embodied robotics, and low-altitude industries. These sectors share technological synergies: intelligent vehicles, robots, and low-altitude systems all depend on intelligent mobility and interaction, built on common AI, energy, and material foundations. Core technologies are transferable across domains—Tesla’s Optimus robot, for instance, shares the same end-to-end neural network training framework and FSD chips as its autonomous driving technology. Supply chains are also highly interoperable, with up to 70% overlap. Chips like NVIDIA’s Orin and Thor serve both autonomous driving and robotics. Application scenarios are also interconnected: drones, robots, and intelligent vehicles can collaborate in inspection, logistics, and mobility to build synergistic ecosystems. Tapping into China’s intelligent vehicle ecosystem can speed up robotics and low-altitude industrialization and boost global competitiveness.

From 2026 onward, convergence will shift from experimentation to deep integration. Automakers will step up expansion into robotics, embodied intelligence, and low-altitude mobility, with early adopters launching small-scale production. Tesla plans to release the third-generation Optimus and start mass production in early 2026. Xpeng’s modular flying car will enter production the same year. GAC’s Aircab flying car will finish certification and launch deliveries, and its GoMate robot will enter commercial use. Changan aims to unveil its first passenger flying vehicle and in-car robotic components.

Meanwhile, suppliers are building second growth curves via “one-to-many” strategies. In 2025, robot-related revenue at top LiDAR firms like HESAI and RoboSense soared over 600% YoY, and robotics is set to take a larger share in 2026. Horizon Robotics’s Digua Robotics products are already integrated into over 100 consumer smart devices, and its 560 TOPS S600 platform will focus on the high-compute embodied robotics segment.

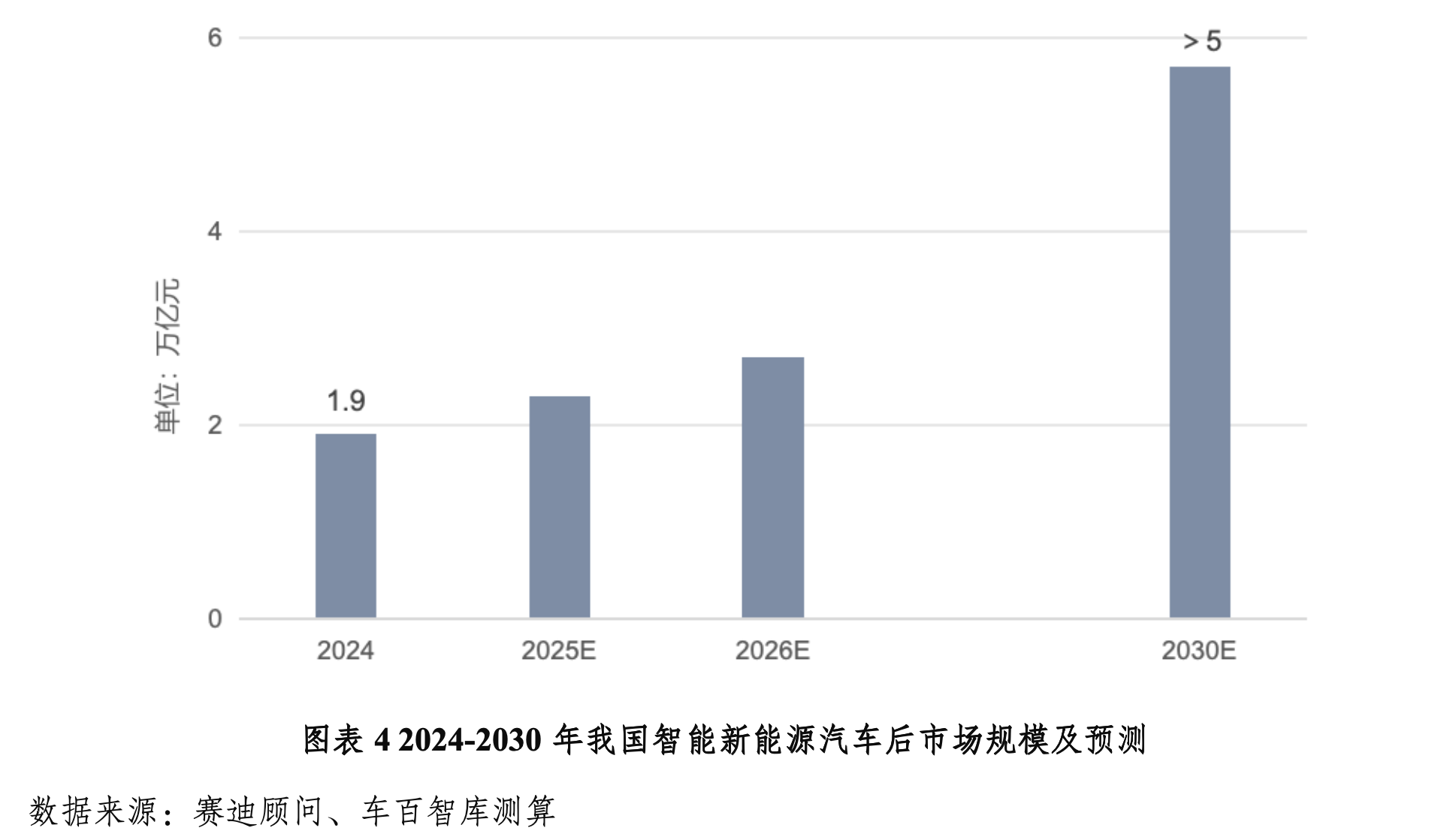

11. New Service Models Become a Strategic Growth Track

As the auto industry moves toward service-focused aftermarket models, its addressable market is growing fast. In 2024, China’s intelligent NEV aftermarket reached around RMB 1.9 trillion and is projected to exceed RMB 5 trillion by 2030. The core shift is from one-time product sales to full-lifecycle services, with profit models moving from manufacturing-driven to “manufacturing + services”—unlocking new value pools.

Intelligent NEV technologies are spawning new service formats across segments. In energy replenishment, V2G is reshaping energy services. By 2030, dispatchable V2G capacity could hit 600 million kWh; integrating V2G with solar-storage-charging and battery-as-a-service (BaaS) will further expand system-level value between vehicles and grids.

In maintenance and repair, digitalization is transforming cars from “hardware products” to “software platforms.” OTA upgrades are now standard: in December 2025, Li Auto launched OTA 8.1, adding 47 new features and optimizing 31 across its MEGA, i, and L series. Remote diagnostics are also reducing costs and improving efficiency—Tesla handled over 2.5 million remote diagnostic sessions in 2024, resolving 200,000+ issues with an average 25-minute turnaround.

In insurance, new technologies and scenarios are reshaping product design and risk modeling. GAC’s Urtrust Insurance launched “Smart Driving Insurance” (up to RMB 3 million coverage) in March 2025; China RE P&C and CPIC introduced low-altitude economy-tailored liability insurance in September 2025.

In parts distribution, big data and blockchain are enabling traceable, trusted supply chains. Tuhu partnered with Huawei Cloud to roll out “one-part-one-code” traceability in May 2024; Wuxi’s Auto Data Space (built by Xing Tong Lun Shu Le) became China’s first trusted auto parts data space in August 2025.

AI is also transforming aftersales. Intelligent customer service and centralized operations are drastically improving responsiveness—AITO’s DMO runs 24/7, handling routine inquiries instantly and escalating complex issues to human agents.

12. Policy Shifts Toward Stronger Regulation and Consumption Support

A high-standard, well-regulated, rules-based policy framework is critical to tackling three key challenges amid rapid transformation. First is safety. With NEV ownership poised to exceed 60 million units, risks have risen from individual to public safety issues. Product standards need strengthening, life safety red lines enforcing, and consumer rights protecting.

Second is development quality. To address excessive competition and involution, policies should guide enterprises toward self-discipline, away from extensive growth, and toward technology- and value-driven development.

Third is regulation. As L3 autonomy and other new technologies near deployment, regulators must strike a precise balance between innovation and risk control, putting in place forward-looking safety assessment and market entry mechanisms.

On the demand side, consumption policy is moving from short-term subsidies to systematic optimization of the NEV usage ecosystem—building a sustainable growth driver. One priority is unlocking lower-tier and rural markets. Rural car ownership is just 42 vehicles per 100 households—far below the urban 81. NEV penetration in rural areas was under 30% in 2024, leaving huge growth potential. Coordinated action is needed on purchase cost reduction, product adaptation, infrastructure coverage, and vehicle-energy integration.

Another priority is building a full-lifecycle usage ecosystem while fostering new industries and formats. This includes accelerating urban-rural charging networks with forward-looking planning; integrating transport and energy infrastructure; boosting maintenance, finance, and insurance innovation; expanding professional, digital aftermarket services; using AI and platforms to improve efficiency and user experience; and nurturing multidisciplinary talent in repair, finance, and data security. Together, these measures will create a high-efficiency, sustainable, end-to-end service ecosystem for China’s new-energy and intelligent vehicle era.